HOW DID WE ATTAIN IT?

CONSTRUCT

PRIMARY CHALLENGE

OTHER FEATURES THAT MAKE THE SYSTEM EFFICIENT FOR MVP

We conducted NAVI business and credit teams to understand the current process of policy creation. Later in the process we conducted sessions with under wroting team to understand how they operate with similar use cases.

Offline process is prone to errors. Due to major is undocumented it leads to error sometimes

No major competitor in market for market analysis

Policies can't be duplicated or reused without rework.

Difficult to audit as the process lacks versioning

Policies once coded can't be edited easily. It has to be redone again by tech team.

Credit policies from co-lenders are submitted to Navi as Word docs or Excel/Google Sheets

UNDERSTANDING CURRENT JOURNEY

Check full co lending flow here

Current shared doc for policy creation

Simplifying the lending process for Navi lending partners

KEY TAKE AWAYS

How might we digitise the current offline process while maintaining familiarity for users?

The challenge lies in finding ways to translate the current doc policies in digital format ensuring that users can easily adapt to the new system without significant relearning.

Make it go live as soon as possible to ship faster, learn faster and finally launch to co-lenders.

Design challenge

Frame

Rule group

Rule

Three major components are

Frame

Rule Groups

Rules

Rules are the atoms and define the entire policy.

Rules groups and frames comply

rules in a framework.

To replicate the current process, we aimed to identify the most easily adaptable approach. We drew inspiration from our internal underwriting team and, after analyzing multiple policies, determined that a complex nesting framework is unnecessary.

For the MVP, we will utilize a straightforward AND/OR framework to streamline the design.

Complexity of nesting.

To address this for our MVP, we implemented a simplified constraint:

When a user selects a combinator (AND/OR) for the entire frame, that combinator will apply uniformly throughout the frame.

Within each frame, rule groups will also adhere to the chosen combinator (AND/OR) consistently when adding additional rule groups.

Similarly, within a rule group, once the user selects a combinator (AND/OR), all subsequent rules in that group will follow the same combinator.

This approach ensures a streamlined and consistent user experience, reducing complexity and enhancing usability.

Frames contains rule groups and rule groups contains rules.

Navi is a tech-driven finance company focused on young middle-income individuals. We provide digital services in insurance, lending, and asset management.

ABOUT NAVI

WHAT IS COLENDING?

WHY DO WE NEED A NAVI LENDING CLOUD?

MY ROLE

Individual contributor

🙋🏻♀️

I worked closely with the content, product, and engineering teams to build Navi lending cloud.

Co-lending is when multiple lenders work together to give loans, like friends chipping in to help you borrow money. This makes it safer for each lender because they share the risk.

Each lender sets their own rules for the loan, and by teaming up, they make lending more diverse and efficient, benefiting the borrower.

The customer wants a loan and applies for a loan at the navi app by filling out basic details like name, address, PAN details, income, and employment information.

1

Both Navi and the co-lender review the customer's application simultaneously, ensuring a thorough yet swift assessment.

3

The approved loan amount is disbursed directly to the customer's bank accoun

4

How does Navi co lend?

Context

The co-lending process involves multiple teams and detailed documentation with fixed processes. To streamline the process and make systems smarter to communicate Navi lending cloud was crafted.

EFFICIENCY / SPEED / TAT

Reduce Turnaround Time (TAT) for deals from weeks to significantly shorter durations.

High reliance on human touchpoints, leading to inefficiencies.

Lack of cohesion among Navi teams and co-lenders.

INDUSTRY TERMS FOR REFERENCE

Internal filtering

Before a loan is passed through the credit policy, the policy created by the lender is replicated by Navi adding few more Navi checks to filter out loans for co-lending and restrict data sharing

Variable creation

For policies to exist, they need a variable. Variables are the backbone of a policy. For example- age is a variable for a policy which can be customised for individual policies.

PRODUCTIVITY

A platform for sending coded policies for lender approval

Platform for lenders to download required reports regularly.

UNIQUE SELLING PROPOSTION

Creation of a USP positioning Navi as a trusted fintech company in the market

To transform an entirely offline relationship into a streamlined online platform.

Ho

HMW enable co-lending business partners to create, explore, and refine policies, ultimately creating a final one for the deal with enabled backtesting.

The motivation behind giving co-lender was primarily to help make NLC self-serve.

The aim was to onboard co-lenders on NLC to create custom variables, make credit policies independently, and see how their policies would perform on Navi customers.

to solve for

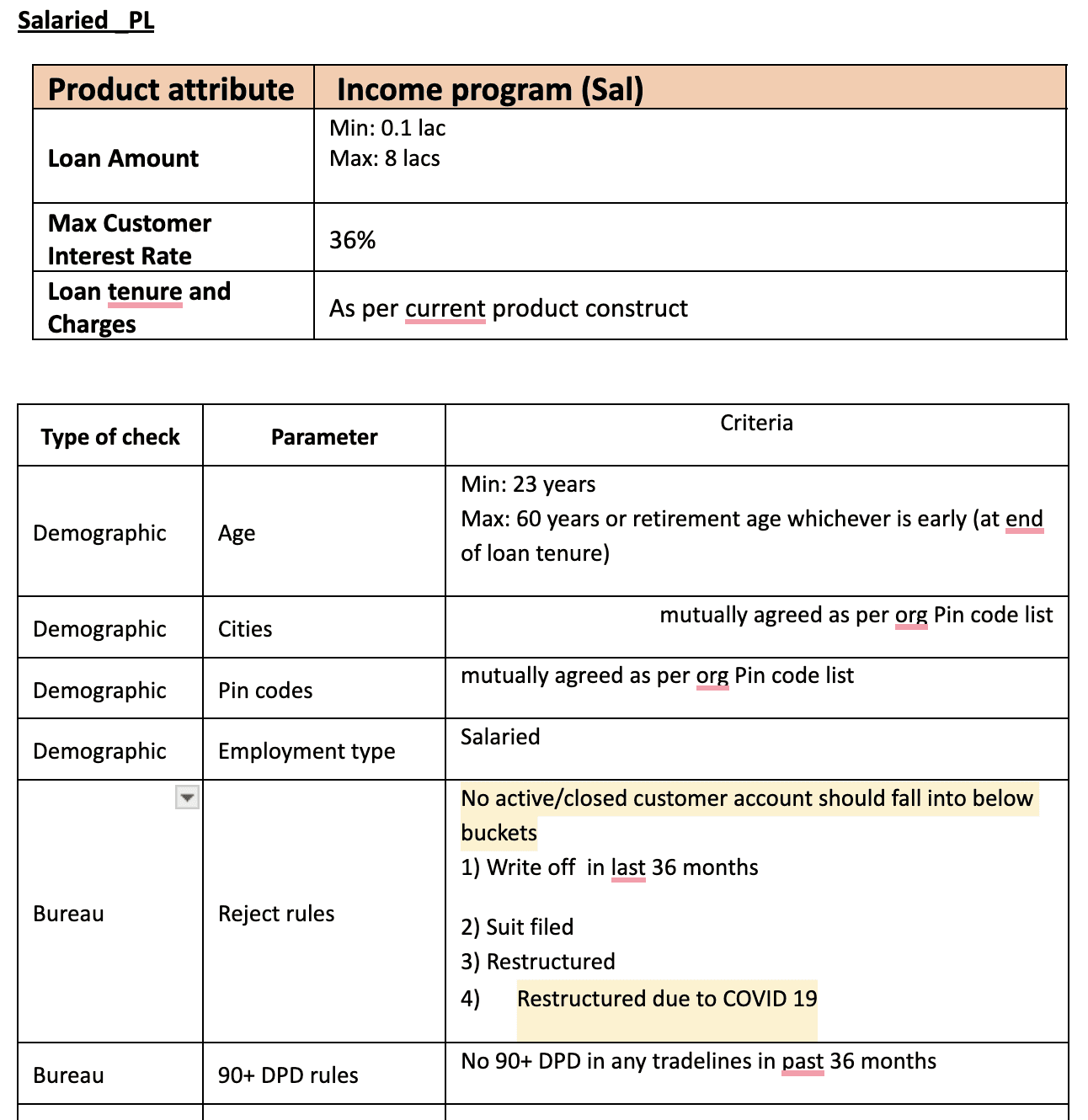

Credit policy

A credit policy is like a set of guidelines that companies follow to decide who they can lend money to It helps them make smart choices about giving credit to customers.

Backtesting

After creating a policy, old loans are tested on this policy to find a drop-off per cent and subsequently relax rules with the backtesting data.

IMP for this case study

Navi pairs the customer with a co-lender based on their

eligibility and requirements

Eligibility and requirements are set of guidelines that Co-lender follow to decide to who they can lend money to it helps them make smart choices about giving credit to customers

Guidelines are communicated via a framework called credit policy.

Navi creates its similar guidelines called as internal filtering

2

Problem statement

Solution

Visual results

For internal users (Navi’s business, product, tech and analytics team)

How might we decrease dependency on/involvement of internal teams w.r.t. co-lender credit policies requirements?

How might we help Navi’s co-lending business reach the goal of 15 co-lenders by the end of 2023 faster?

For external users (Co-lender credit & risk teams)

How might we give co-lenders more autonomy and flexibility to create and test multiple credit policies in a shorter amount of time?

How might we allow co-lenders to make informed decisions on their credit policies to help meet their business standards and requirements

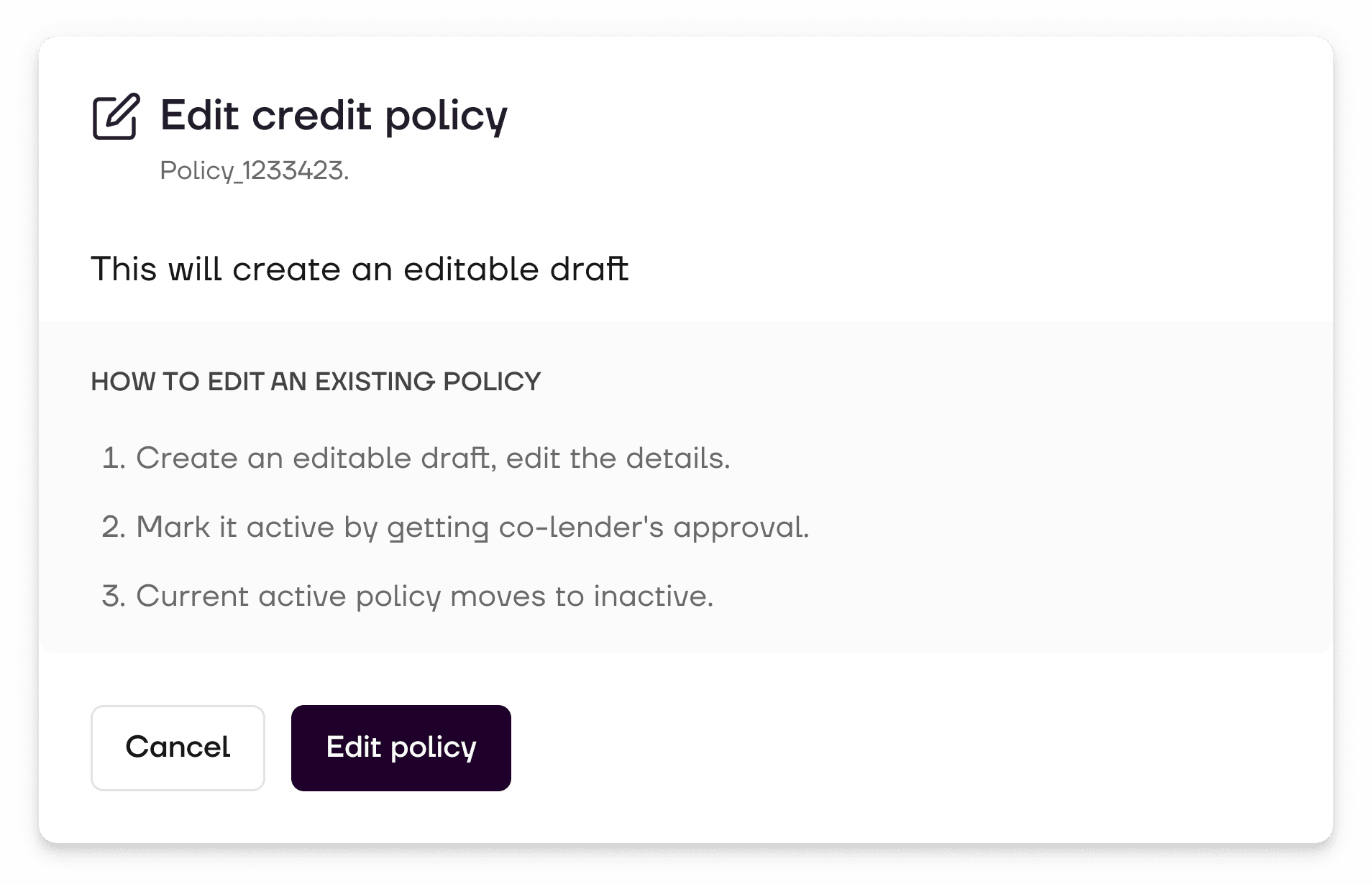

Once a policy is created by the Navi business team, it is sent for approval to co-lenders to check and approve. Once approved it is attached to a deal and loans are processed thereafter

APPROVAL OF A POLICY

Policies created once can be reused with little tweaks for another deal.

To support this we created a clone feature

Navi business teams can clone polices as credit or internal filtering for the current organisation or even another organisation

CLONE OF POLICY

Policies created once can be reused with little tweaks for another deal.

To support this we created a clone feature

Navi business teams can clone polices as credit or internal filtering for the current organisation or even another organisation

EDIT OF POLICY

Impact

Multiple other features we have made live by now

Currently, NLC is utilised by Navi internal teams and three co-lender organisations, with policy creation in the testing phase.

We have significantly reduced the turnaround time (TAT) for policy creation from weeks to days, facilitating faster iterations and quicker deployment.

Additionally, testing with co-lenders is ongoing, focusing on refining Navi Lending Cloud's policy creation process and other aspects to ensure a seamless user experience.

VARIABLE CREATION

REIMAGINED USER FLOW

Variables are what make a policy, users will tweak variables for a policy. Values of a variable define the policy constraints

We have few computed variables which need a switch off/ on.

Rest are derived from backend but user can make multiple customisation of each variable.