Effortless personal loan

repayment, tracking and

managment

OVERVIEW

Navi's core offering is the Navi personal loan. As of March 31, 2023, Navi Finserv Limited had disbursed 1,870,683 personal loans totaling ₹11,500.41 crore, with an average loan size of ₹61,477.

I worked on multiple small and mid size features for Navi personal loan- post purchase experiences

my role

Research, Analysis, Product Design, Dev-of

TEAM

2 Product Managers & 10 Engineers

COMPLIANCE

When I moved to the Navi personal loan team, we were in the middle of transitioning our app to a web-based experience to comply with RBI regulations. This was a major change in the user experience, but it was necessary for compliance. The transition required developing web screens from scratch within limited timelines. We had to prioritize essential features to meet the compliance deadlines while ensuring a smooth user experience across both the web and app platforms. Despite the time constraints, we managed to maintain design consistency and core functionality during the transition.

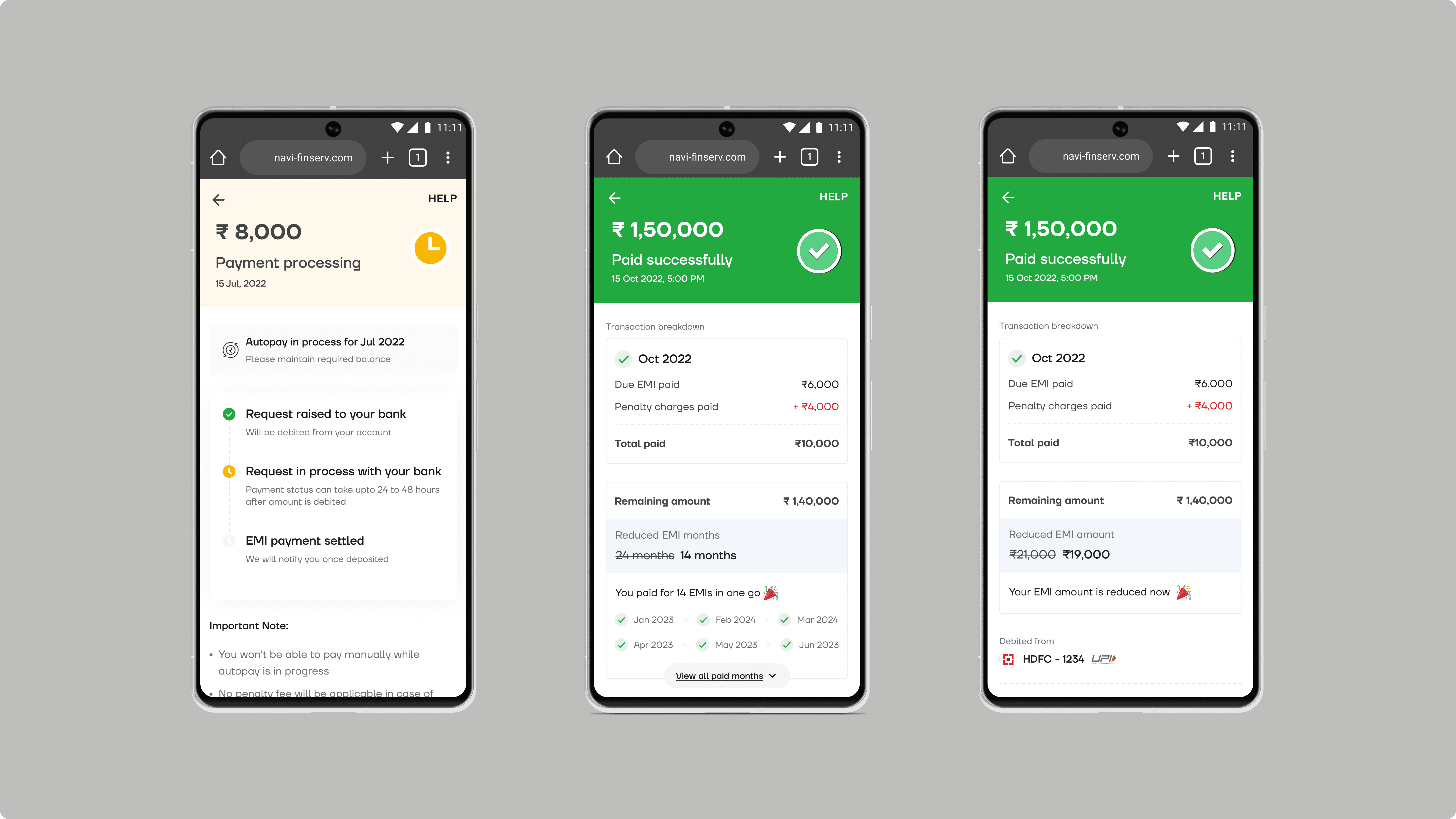

TRACKING OF REPAYMENT

For a long time, there was no clear way for users to track how their loan repayments were being adjusted, which led to confusion and dissatisfaction.

Users were unaware of how extra payments were being applied — whether they were reducing loan tenure or reducing EMI amounts.

By default, the system was set to reduce the tenure, which created confusion when users expected their EMI amounts to decrease. This issue was further compounded when users expected future EMIs to be covered by extra payments, only to realize that the payments were being applied to the last EMIs of the loan tenure instead.

To resolve this, we introduced a second-level (L2) page following the transaction listing page. This page explained how the money was being adjusted and provided a clear view of which EMIs were paid off using the extra amount. We also added a new repayment calendar that reflected the updated payment schedule, helping users understand how future payments would be affected. This improved transparency reduced confusion and increased user confidence in the repayment process.

a

PART PRE PAYMENT AND ITS CONFUSION

we get 150-200 tickets a day for this, its when user pays extra and Users were unaware of how the money repaid is getting adjusted as with part pre-payment users were able to pay extra amount to either reduce tenure or reduce emi- but with current expereince default reduce tenure was selected which confused users post the payment was made; the other catch was as user expects the next emis to be paid off, the last emis of tenure getd paid which creates a lot of confusuin for users.

many tickets are also becuase users dont know how much can they pay and if they pay how will t convert into less emi or tenure?

CLOSED LOANS

Navi has 60% repeat users and has one or more closed loans with us, but we didn't cater to any closed loan information for the users.

We had an average of 15-20 tickets a day for closed loans information, which didn't make it a burning issue but was still a pain point!

We rolled out a closed loan feature which holds user's all closed data.

Learnings and Reflection